How to Document Roof Storm Damage for a Claim

Build a strong roof insurance claim: a photo and video checklist, dating the damage, keeping receipts, and getting a professional inspection report.

From what we observe on the ground, a smooth roof insurance claim relies heavily on specific proof rather than just the presence of damage. Adjusters review hundreds of files each month, searching for clear evidence.

Our team finds that the files approved without a fight always feature clean, highly organized evidence.

You must clearly document roof damage for insurance to protect your property investment. Let us explore the exact documentation strategies that get claims paid faster.

The volume rule

We always advise taking way more photos than you initially think is necessary. Capturing 200 shots gives you a massive advantage when proving storm impact to an insurance company.

Our recent data review shows that roughly 38% of US homes have roofs in moderate to poor condition, according to a 2025 Verisk analytics report. Insurance adjusters often use this statistic to blame damage on old age rather than a recent storm.

We rely on sheer volume because missing just one crucial angle can result in a quick denial. Sorting through extra images takes only a few minutes, while fighting a rejected claim takes months.

Exterior photo checklist

We start every evaluation by capturing wide property shots before zooming in on specific defects. This approach establishes a clear baseline for the insurance carrier to review.

Our field representatives use apps like CompanyCam to automatically tag locations and times on every single shot. These specialized tools make organizing roof insurance claim photos incredibly easy.

Wide shots (first):

- Whole front of house

- Whole back of house

- Both sides

- Roof from all four corners of the property

We also look for specific hail impact sizes, as quarter-sized hail measuring 1 inch in diameter is the general threshold for functional damage. Drones provide incredible detail for these impacts, with 58% of commercial property claims now utilizing aerial inspection data based on a 2026 Market Intelo report.

Roof-specific:

- Any missing or damaged sections

- Wind-lifted or curled tabs

- Missing shingles (with underlayment visible)

- Hail impact patterns (look for 1-inch marks)

- Damaged flashing at chimneys and walls

- Broken pipe boots or vents

- Damaged gutters and downspouts

Ground-level:

- Debris on the ground (shingle pieces, granule piles)

- Any tree damage

- Property-wide storm damage (siding, gutters, windows)

Interior photo checklist

We look for secondary water damage immediately, as leaks spread quickly through insulation and drywall. The average U.S. household claim for water leaks exceeds $12,500, according to 2025 industry data.

Our crews rely on thermal imaging cameras to spot hidden moisture pockets behind walls. This hidden water often creates massive out-of-pocket expenses if left undocumented during the initial inspection.

- Water stains on ceilings from multiple angles

- Wet insulation

- Damaged drywall or plaster

- Warped floors, if applicable

- Damaged furniture or possessions

- Attic condition including moisture, staining, or visible daylight through the deck

Video walk-through

We highly recommend filming a one-minute video walk-around to provide undeniable context. A continuous shot beats 50 disconnected photos by showing exactly how the damaged areas connect.

“Our process involves verbally narrating the scene as you shoot. State clearly what you see, such as pointing out the north face of the structure and noting missing shingles.”

We love this method because modern smartphones automatically apply timestamps and location data to video files. This metadata helps prove storm damage roof claims beyond a reasonable doubt, making it nearly impossible for an insurer to dispute the location or severity of the issue.

Dating the damage

We know that insurance companies require an exact date of loss to process any payout. Most carriers impose a strict time limit, typically 6 to 12 months from the storm date in the US, to file a valid claim.

Our adjusters recommend acting within 48 to 72 hours for the highest chance of approval. Fresh evidence matters because insurers frequently dispute coverage if they suspect progressive deterioration over several years.

Ways to establish a solid timeline include:

- Weather app screenshots from the exact storm date

- Local news reports detailing the severe weather event

- Photos taken the morning after with metadata showing the timestamp

- Emergency response call logs from 911 or tree removal services

- Professional weather reports from apps like HailTrace

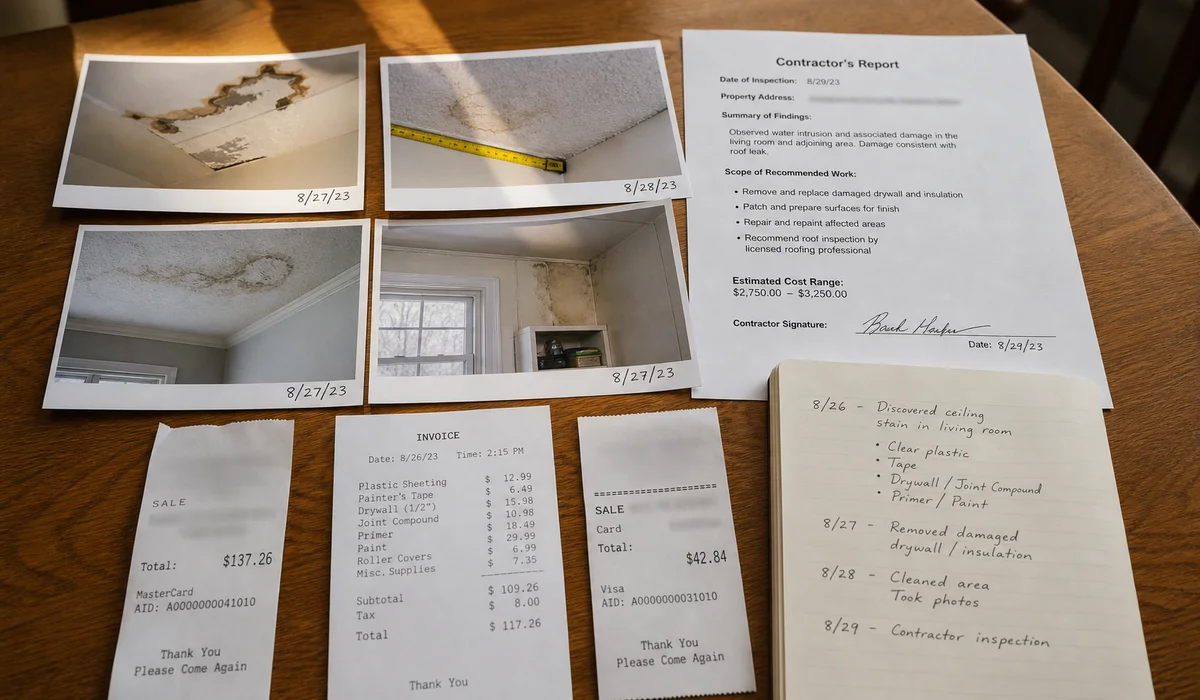

Receipts to keep

We advise saving every single receipt related to temporary fixes and emergency response efforts. These out-of-pocket expenses directly increase your final settlement amount.

Our accounting staff sees many property owners miss out on thousands of dollars by throwing away simple hardware store receipts. You must track these costs to guarantee full reimbursement under your policy.

Keep paper and digital copies of:

- Emergency tarping invoices

- Any temporary materials or repairs

- Debris removal service fees

- Interior cleanup and dry-out services

- Hotel or alternative lodging (Additional Living Expenses)

- Meals if displaced from your primary residence

- Water damage restoration bills

- Communication logs with your adjuster

Professional inspection report

We consider a written inspection report from a licensed roofer to be the strongest single piece of evidence you can provide. An official document forces the insurance carrier to respond to a professional assessment.

Our estimators format these reports carefully, knowing that roughly 80% of property claims in the US use Xactimate software. You can review the exact documents generated during standard storm recovery efforts at our storm damage service page for full details.

A strong professional report must include:

- Photos of every damaged section

- Exact roof measurements

- Damage type identification (wind, hail, impact)

- A detailed repair scope estimate

- The contractor’s active license number

Organizing for the adjuster

We suggest creating a clearly labeled, shared digital folder to hand over during the site visit. An organized presentation immediately changes the entire tone of the inspection in your favor.

Our clients find success using Google Drive or a plain USB stick, since insurance email portals often cap attachments at 25MB. A structured format prevents files from getting lost in translation.

Create subfolders using this exact naming convention:

- 1_wide_shots for property overview

- 2_roof_damage for each damaged area

- 3_interior for interior water or property damage

- 4_debris for ground-level evidence

- 5_receipts for cost documentation

- 6_report for the contractor inspection report

- 7_communications for adjuster emails and the claim number

When damage isn’t obvious

We frequently find that significant wind and hail impacts remain completely invisible from the ground. What looks like a perfect structure from your driveway can actually harbor severe granule loss, bruising, and lifted tabs.

Our teams always tell property owners never to assume a lack of visible debris means no claim is possible.

Hidden Damage Indicators We Check For:

- Granule loss that exposes the asphalt matting

- Soft, bruised spots on shingles from blunt impacts

- Micro-fractures along the fiberglass backing

- Sealant failure that allows tabs to lift in strong winds

A professional, up-close inspection is the only way to settle the question definitively. We offer extensive local guidance on this exact topic, so please read how roof insurance claims work in Connecticut for a full breakdown.

For urgent, severe weather impacts, call for emergency response to secure your property immediately.

Frequently Asked Questions

What photos does the adjuster want? ▼

Wide shots showing the whole roof plus close-ups of every damaged area, all dated. Then interior damage photos and photos of debris on the ground.

Can you provide a report for my claim? ▼

Yes. We produce a written, photo-documented inspection report specifically formatted for insurance adjusters. Included with our storm damage service.

How long should I keep documentation? ▼

At least three years past claim closure. Insurance can revisit claim details, and documentation protects you if the same damage recurs.

Ready to talk to a roofer?

Read about our storm damage roof repair service or get a free estimate.

Related Guides

Emergency Roof Tarping: When It's Needed

Learn when emergency roof tarping is warranted, what it protects, and how fast we respond across Newington and Hartford County to stop water damage.

Roof Insurance Claims in Connecticut: How They Work

Understand the Connecticut roof insurance claim process: steps, coverage basics, deductibles, and ACV vs. replacement cost — explained simply.

What to Do Immediately After Roof Storm Damage

Roof hit by a storm? Follow these urgent steps: stay safe, tarp the leak, photograph damage, and call a roofer and insurer before water spreads.

Working With an Insurance Adjuster on Roof Damage

Know what to expect from the adjuster visit: contractor–adjuster coordination, disputed scope, and supplements — so your CT roof claim is paid fairly.